What is Cash Flow-Direct vs. Indirect Method

✅ Information Verified by a CPA

Cash flow is the lifeblood of any business, but for construction firms, it can be the difference between staying solvent and struggling to meet payroll. Projects involve long timelines, delayed payments, and fluctuating expenses. Revenue alone doesn’t tell the full story, it is important to understand how cash moves in and out of your business.

Understanding cash flow helps businessowners and operators to make informed decisions: whether it’s taking on a new project, managing subcontractor payments, or planning for seasonal slowdowns. However, many firms rely solely on traditional profit and loss statements, overlooking the insights a cash flow statement can provide.

This article breaks down the direct and indirect methods of cash flow reporting, explains how they differ, and highlights practical ways construction leaders can use them to keep their operations financially healthy and predictable.

What is Cash Flow: Understanding the basics

Cash flow is the movement of money in and out of a business over a specific period. Unlike profits, which are based on accounting rules and often include non-cash items like depreciation, cash flow shows the actual liquidity available to pay bills, employees, and suppliers.

For construction firms, this distinction is critical. A job or a project looks profitable on paper but is unpredictable due to slow payments and unexpected material costs that create a cash shortfall.

Cash flow is typically divided into three categories:

- Operating Cash Flow—Money generated or used in day-to-day operations, like receiving payments from clients and paying subcontractors.

- Investing Cash Flow—Cash spent on or received from long-term investments, such as purchasing equipment or selling assets.

- Financing Cash Flow—Cash related to funding the business, including loans, equity injections, or dividend payments.

With this flow, construction leaders get a clear picture of questions like

- Can I afford to start a new project next month?

- Do I have enough liquidity to weather seasonal slowdowns?

- Where are the bottlenecks in my cash management?

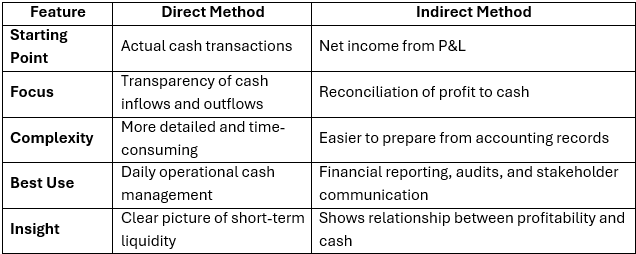

Direct Method of Cash Flow

The direct method lists actual cash inflows and outflows from operations. It answers a straightforward question: “Where is my cash coming from, and where is it going?”

For a construction business, this method tracks things like

- Payments received from clients for completed projects

- Cash paid to subcontractors and suppliers

- Payroll and overhead costs

Direct cash flows don’t start from net income; they start with real cash transactions. This makes it highly transparent, which is why some CFOs prefer it when they need to understand daily liquidity clearly.

Advantages of the Direct Method:

- Clear visibility—you can see exactly which payments are coming in and which are leaving.

- Better cash management—easier to plan for upcoming payments or potential shortfalls.

- Useful for internal decisions—helps project managers and finance teams identify timing issues with receivables or payables.

Let’s understand by an example:

Imagine a roofing company that completed three projects last month:

- Received $50,000 from Project A, $30,000 from Project B, and $20,000 from Project C

- Paid $40,000 to subcontractors and $10,000 in overhead

Using the direct method, the cash flow statement would show an operating inflow of $100,000 and outflows of $50,000, leaving a net cash inflow of $50,000. This makes it clear how much cash is available to fund the next project or cover payroll.

Indirect Method of Cash Flow

The indirect method takes a different approach. Instead of listing every cash transaction, it starts with net income from the profit and loss statement and adjusts for non-cash items and changes in working capital.

This method is often preferred for reporting purposes because it links accounting profits to cash movements, showing how earnings translate into actual cash.

How it Works:

1. Start with net income from the income statement.

2. Add back non-cash expenses, like depreciation or amortization.

3. Adjust for changes in current assets and liabilities, such as:

a. Accounts receivable (cash not yet collected)

b. Accounts payable (cash owed to vendors)

c. Inventory changes

Advantages of the Indirect Method:

- Shows the relationship between profit and cash, helping identify operational inefficiencies.

- Easier to prepare from standard accounting records, especially for firms already using accrual accounting.

- Commonly used in financial reporting so stakeholders like banks or investors understand your cash position.

Limitations for Construction Firms:

- Less intuitive than the direct method, harder to see day-to-day cash availability.

- Delayed or complex adjustments may make it less useful for short-term operational decisions.

Example in Practice:

A construction company reports a net income of $60,000. During the same period:

- Depreciation expense: $5,000 (non-cash, added back)

- Accounts receivable increased by $15,000 (cash not yet collected, subtracted)

- Accounts payable increased by $10,000 (cash retained, added)

The net cash flow from operations would be $60,000 + $5,000 - $15,000 + $10,000 = $60,000. While net income suggested strong earnings, the adjustments show the real cash position more accurately.

Direct vs. Indirect Method – Key Differences

Both the direct and indirect methods aim to show cash flow, but they do it in very different ways. Understanding these differences helps construction leaders choose the right approach for their needs.

In short, you should:

- Use the Direct Method when you need to track real cash daily or weekly, for example, managing subcontractor payments or planning project expenses.

- Use the indirect method for reporting to banks, investors, or auditors, as it ties cash flow to reported earnings.

Some firms use both methods: direct for internal decision-making and indirect for external reporting.

Which Method Should Construction Firms Use?

Choosing between the direct and indirect methods depends on your business needs, reporting requirements, and operational priorities. There’s no one-size-fits-all but understanding the trade-offs helps business owners.

Consider Your Internal Needs

If your goal is day-to-day cash management, the direct method is often more useful. It shows exactly where cash is coming from and going to, making it easier to:

- Schedule subcontractor and supplier payments

- Forecast short-term liquidity for ongoing projects

- Avoid unexpected cash shortages during slow seasons

Factor in External Reporting

The indirect method is widely accepted for financial statements and audits. If your firm regularly reports to banks, investors, or potential partners, this method aligns better with standard accounting practices and ensures:

- Profit and cash flow reconciliation is clear

- Financial statements are audit-ready

- Stakeholders understand your cash position relative to net income

Evaluate Resource Availability

The direct method requires detailed tracking of every cash transaction, which can be time-consuming without proper accounting software. The indirect method, on the other hand, can be prepared from existing accrual-based records with less effort.

Hybrid Approach

Many construction firms adopt a hybrid strategy:

- Use direct cash flow tracking internally to manage operations and make quick decisions

- Use indirect reporting externally for compliance and stakeholder communication

Conclusion: The Cash Flow Edge

For construction firms, cash flow is more than a line on a financial statement; it is the lens through which the real health of a business becomes visible. Understanding the differences between the direct and indirect methods matters, but the true value comes from acting on that information consistently and strategically.

Direct cash flow insights provide clarity on day-to-day liquidity, making it easier to plan payments, allocate resources, and avoid short-term surprises. The indirect method, meanwhile, offers a broader perspective that stakeholders—lenders, investors, and auditors—rely on to evaluate financial health. When used together thoughtfully, these methods allow firms to connect daily operations with long-term financial strategy, giving leaders confidence in every decision they make.

Cash flow allows teams to anticipate challenges before they impact operations, adjust to seasonal cycles and project delays, and make informed decisions about taking on new work. Book a consultation call with Atheneum and turn financial insights into actionable decisions.

About The Author

Daniel Kaufman, is a CPA with over 20 years of experience helping businesses plan with confidence. He helps business owners understand their financial numbers and make smarter decisions for long-term growth. Daniel specializes in small business tax planning, setting up accounting systems, and is a QuickBooks ProAdvisor. He is passionate about giving business owners clarity and confidence through better financial insights.

FAQs

What is the difference between the direct and indirect methods of cash flow?

The direct method lists actual cash inflows and outflows from operations, showing exactly where cash is received and spent. The indirect method starts with net income and adjusts for non‑cash items and working capital changes to arrive at cash flow. Both ultimately produce the same net operating cash flow but differ in presentation and detail level.

Which method should my construction business usefor cash flow reporting?

For day‑to‑day liquidity insights, the direct method provides clearer visibility of real cash movements. For external reporting, audits, or stakeholder communication, the indirect method is easier to prepare from existing accounting records and aligns with common financial reporting practices. Many firms use a hybrid approach for internal planning and external reporting.

Does it matter which cash flow method I choose fortotal cash flow results?

No, regardless of whether you use the direct or indirect method, the total net cash from operating activities will be the same. The difference lies only in how operating cash flow is presented not in the final cash position.

Why is the indirect method more commonly used than the direct method?

Most companies prepare financials on an accrual basis, which makes it easier to use the indirect method since it starts with net income and adjusts for non‑cash items. The direct method requires detailed cash transaction tracking, which can be more time‑consuming andresource‑intensive.

Can a cash flow statement prepared using the indirect method help me understand short‑term cash needs?

Yes, but with limitations. The indirect method shows how profit turns into cash, which helps explain changes in cash overtime. However, it may not show the exact timing of receipts and payments,making it less precise for short‑term planning compared to the direct method.

Read More Blogs

Connect with our experienced CFO advisory team

Get Insights

Submit the contact form to receive tailored financial insights and practical guidance from our team

Seamless Experience

Share your needs through the form for quick responses and smooth onboarding support.

Pricing That Makes Sense

After reviewing your inquiry, we provide transparent, practical pricing aligned with your business financial needs.